Getting Started: 30 seconds to InferPy¶

The core data structures of InferPy is a probabilistic model, defined as a set of random variables with a conditional independence structure. Like in Edward, a random varible is an object parameterized by a set of tensors.

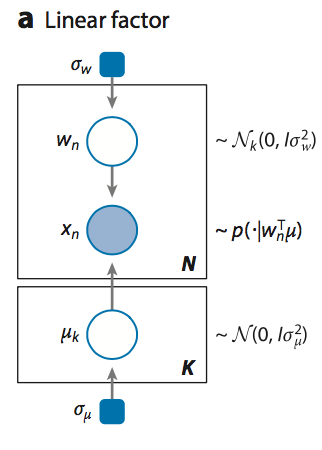

Let’s look at a simple (Bayesian) probabilistic component analysis model. Graphically the model can be defined as follows,

Bayesian PCA

We start defining the prior of the global parameters,

import numpy as np

import inferpy as inf

from inferpy.models import Normal, InverseGamma, Dirichlet

# K defines the number of components.

K=10

# d defines the number of dimensions

d=20

#Prior for the principal components

with inf.replicate(size = K)

mu = Normal(loc = 0, scale = 1, dim = d)

InferPy supports the definition of plateau notation by using the

construct with inf.replicate(size = K), which replicates K times the

random variables enclosed within this anotator. Every replicated

variable is assumed to be independent.

This with inf.replicate(size = N) construct is also useful when

defining the model for the data:

# Number of observations

N = 1000

#data Model

with inf.replicate(size = N):

# Latent representation of the sample

w_n = Normal(loc = 0, scale = 1, dim = K)

# Observed sample. The dimensionality of mu is [K,d].

x = Normal(loc = mu0 + inf.matmul(w_n,mu), scale = 1.0, observed = true)

As commented above, the variable w_n and x_n are surrounded by a

with statement to inidicate that the defined random variables will

be reapeatedly used in each data sample. In this case, every replicated

variable is conditionally idependent given the variables mu and sigma

defined outside the with statement.

Once the random variables of the model are defined, the probablitic model itself can be created and compiled. The probabilistic model defines a joint probability distribuiton over all these random variables.

from inferpy import ProbModel

# Define the model

pca = ProbModel(vars = [mu,w_n,x_n])

# Compile the model

pca.compile(infMethod = 'KLqp')

During the model compilation we specify different inference methods that will be used to learn the model.

from inferpy import ProbModel

# Define the model

pca = ProbModel(vars = [mu,w_n,x_n])

# Compile the model

pca.compile(infMethod = 'MCMC')

The inference method can be further configure. But, as in Keras, a core principle is to try make things reasonbly simple, while allowing the user the full control if needed.

from keras.optimizers import SGD

# Define the model

pca = ProbModel(vars = [mu,w_n,x_n])

# Define the optimiser

sgd = SGD(lr=0.01, decay=1e-6, momentum=0.9, nesterov=True)

# Define the inference method

infklqp = inf.inference.KLqp(optimizer = sgd, loss="ELBO")

# Compile the model

pca.compile(infMethod = infklqp)

Every random variable object is equipped with methods such as

log_prob() and sample(). Similarly, a probabilistic model is also

equipped with the same methods. Then, we can sample data from the model

anbd compute the log-likelihood of a data set:

# Sample data from the model

data = pca.sample(size = 100)

# Compute the log-likelihood of a data set

log_like = probmodel.log_prob(data)

Of course, you can fit your model with a given data set:

# Fit the model with the given data

pca.fit(data_training, epochs=10)

Update your probablistic model with new data using the Bayes’ rule:

# Update the model with the new data

pca.update(new_data)

Query the posterior over a given random varible:

# Compute the posterior of a given random variable

mu_post = pca.posterior(mu)

Evaluate your model according to a given metric:

# Evaluate the model on given test data set using some metric

log_like = pca.evaluate(test_data, metrics = ['log_likelihood'])

Or compute predicitons on new data

# Make predictions over a target var

latent_representation = pca.predict(test_data, targetvar = w_n)